One after another, the market keeps on breaking records. So far in 2019, the S&P 500 has rallied 24%, the Nasdaq has been lifted 29% and the Dow Jones has jumped 20% higher. Gains from Nasdaq heavy weights Tesla, Facebook and Broadcom sent the index soaring yesterday while the Dow was weighed down from its all-time highs by reduced full-year forecasts from major U.S. retailers.

Given the Dow’s fall from grace, investors have been left wondering what this rally, which was largely driven by better-than-expected third quarter earnings results as well as a more optimistic outlook on trade, means for stocks.

Morgan Stanley’s chief U.S. equity strategist Michael Wilson believes the market will keep climbing higher. “Our economists think the U.S. will avoid a recession next year, thanks to swift action by the Fed and improving trade tensions,” he commented. However, he notes that consecutive quarters of earnings declines are likely.

As a result, some have expressed concern that as the market skyrockets, equity valuations are becoming too steep especially with low expectations for future earnings as well as the fact that a U.S.-China deal has yet to be signed. Tightening credit conditions, which can be a sign that the economy is heading for trouble within the coming months, the condition of the yield curve and uncertainty regarding the U.S. Presidential Election in 2020 have also sounded alarm bells.

Against this backdrop, the U.S. Commerce Department reports that corporate profits have fallen flat since 2014, while bond yields have taken a serious hit.

“During the last year, the S&P 500 trailing 12-month earnings per share has been essentially flat but the 10-year bond yield has collapsed. That is, growth of the future dividend stream has been compromised but the discount rate of future cash flows has been significantly reduced,” Leuthold Group chief investment strategist Jim Paulsen wrote. Additionally, he points out that while the market’s valuation is also on the rise, this isn’t necessarily a bad thing.

“Investors do not often get to enjoy a halving of the long-term cost of capital without a more significant decline in corporate earnings,” Paulsen explained.

Taking all this into consideration, we wanted to take a closer look at 3 stocks that can’t seem to avoid Wall Street’s attention recently. To do this, we turned to the Street’s seasoned analysts in order to go beyond all the headlines.

Here’s the scoop on these 3 trending stocks.

Advanced Micro Devices, Inc. (AMD)

The semiconductor company has made quite a bit of noise on the Street thanks to its new product launch. Yesterday, AMD released its 7nm Radeon Pro W5700 graphics cards, sending shares up 4%.

The highly buzzed about graphics cards are powered using the company’s innovative RDNA architecture and are widely considered to be a huge step-up from the previous generation as they offer 1.25 times the instructions per clock. Starting at a $799 price point, the W5700 was designed with engineers, 3D designers and architects in mind.

AMD maintains that 2020 will be the “year of mobile Ryzen” as several other 7nm products are unveiled across all markets over the next six months, de-emphasizing the low-end CPU market, which has been a staple in the business. Rosenblatt Securities analyst Hans Mosesmann argues that this shift should bode well for AMD. “We see the company’s relative advantage significantly better than in desktops given the need for performance, core-counts, efficiency and battery life,” he wrote in a note to clients. With the company also making progress in the GPU compute space as a result of partnerships with key players like Google, the five-star analyst remains with the bulls. At a price target of $52, Mosesmann thinks shares could surge 26% over the next twelve months. (To watch Mosesmann’s track record, click here)

Meanwhile, Mizuho Securities’ Vijay Rakesh sees the intense competition from Intel as a steep hurdle for AMD to overcome. Even with its new graphics cards, the five-star analyst argues that AMD is being undercut by Intel’s Cascade Lake price reduction. He adds that Intel has also been aggressive in terms of offering software support. To this end, he reiterated his Hold rating and $38 price target, indicating 8% downside. (To watch Rakesh’s track record, click here)

Looking at the consensus breakdown, Wall Street’s take is varied. 12 Buy ratings, 10 Holds and 1 Sell received over the last three months add up to a ‘Moderate Buy’ Street consensus. With a $37 average price target, the downside potential comes in at 11%. (See AMD stock analysis on TipRanks)

Qualcomm Inc. (QCOM)

For the other semiconductor stock on our list, Qualcomm, it was its three-year targets that captured Wall Street’s attention.

Shares dipped 3% lower yesterday after the company provided updated guidance during its Analyst Day event. Management stated that growth in its serviceable addressable market (SAM) from $65 billion in 2019 to $100 billion in 2022 could be driven by an overall Qualcomm CDMA Technologies (QCT) SAM CAGR of approximately 10%. Investors also learned that QCOM believes QCT growth will be greater than the SAM growth plus incremental Apple revenue. In terms of operating margins, QCT could land at more than 20% with Qualcomm Technology Licensing (QTL) potentially coming in at 70%.

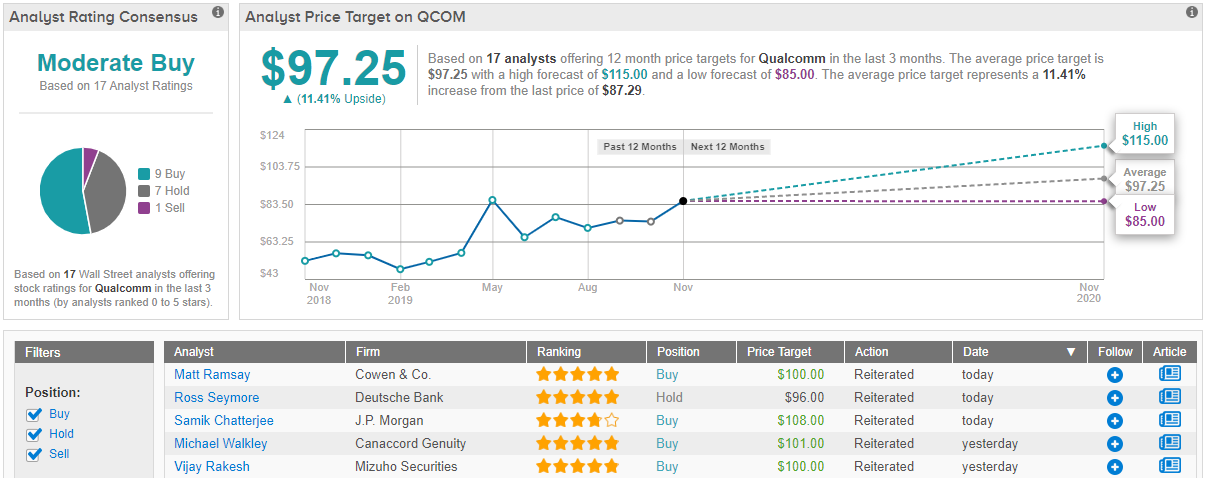

Canaccord Genuity analyst Michael Walkley tells investors that he views these targets as achievable based on its ability to maintain the QTL growth trajectory and its potential to take 5G market share. He cites QCOM’s 300 license agreements to-date including over 75 for 5G and multi-year agreements signed with “anchor” customers like Apple to back up this conclusion.

“We believe our estimates will remain above consensus for F2020 and F2021 given our belief the ramp of 5G will drive a strong increase in revenue per MSM and overall stronger results and margin leverage for as 5G ramps,” he commented. As a result, the five-star analyst kept his Buy recommendation and $101 price target. This suggests that there’s room for 15% upside from the current share price. (To watch Walkley’s track record, click here)

When it comes to other analysts’ takes on QCOM, the consensus is split. With 9 Buys, 6 Holds and 1 Sell issued in the previous three months, the chip stock is a ‘Moderate Buy’. In addition, the potential twelve-month gain is 11% based on the $97 average price target. (See Qualcomm stock analysis on TipRanks)

Slack Technologies (WORK)

Slack was just dealt a major blow by its competitor Microsoft. On the heels of the news that Microsoft’s competing product, Teams, expanded its daily active user (DAU) count from 13 million in July to 20 million current DAUs, or 54% growth in less than six months to be exact, Slack shares slumped 8%.

As Slack had 12 million DAUs in October, it’s no wonder the workplace communication tool provider has been taking heat from investors. Nonetheless, the company points out that in terms of DAUs, the most important factor to consider is engagement. Management noted, “Deep and sustained levels of engagement across companies are what keep people adopting Slack and using it above other, less connected ways of working.”

However, the fact of the matter is that even if Slack’s DAUs are more “active” than Microsoft’s, the gap between the two has grown too large to ignore. This is the stance taken by Wedbush analyst Daniel Ives, who views Teams as posing a huge threat to Slack.

“Increasing user productivity and optimizing an organizations work flow through internal messaging plays right into the sweet spot for Microsoft and we find it very hard to believe any competition could displace the current dominance of the Office 365 product suite with our estimation that only 10%-15% of the core Microsoft enterprise customer base is potentially in play for Slack to likely go after in collaborative bakeoffs based on our field checks,” the four-star analyst explained.

With this in mind, Ives initiated coverage by publishing a bearish call and setting a $14 price target. This target demonstrates significant downside potential of 34%. (To watch Ives’ track record, click here)

Based on the 7 Buys, 7 Holds and 1 Sell assigned in the last three months, the word on the Street is that Slack is a ‘Moderate Buy’. At an average stock-price forecast of $31, the upside potential comes in at 46%. (See Slack stock analysis on TipRanks)